In the evolving landscape of global online video services, 30A Media emerges as a leading developer for FAST and VOD streaming apps. Omdia analyst Adam Thomas delves into the numbers, shedding light on the future of the industry.

The past year marked a significant shift in the online video sector. The industry’s focus shifted from relentless pursuit of subscription growth to a more prudent approach centered around profitability. This change was catalyzed by the unprecedented subscription losses experienced by Netflix in the first half of 2022.

Against this backdrop, the combined global revenue for traditional TV and online video sectors reached a noteworthy $516 billion in 2022. Omdia’s projections indicate this figure is set to rise to $569 billion by 2028, representing a compound annual growth rate (CAGR) of 1.7%. These figures encompass advertising revenue from premium AVOD/FAST services but exclude social video advertising (e.g., YouTube, Meta, TikTok) and other forms of online video advertising (e.g., in-banner video or CTV UI video advertising).

Among the components constituting the TV/video sector, the most rapid growth is observed in ad-supported online video. Its revenue, which stood at $24.6 billion in 2022, is expected to surge at a CAGR of 14.3% to reach $55.1 billion by 2028. Focusing on the paid-for services highlighted in the multisubscription research, online channel (SVOD) services generated $85.5 billion in 2022, with Omdia forecasting an increase to $129.2 billion in 2028 (a 7.1% CAGR).

Conversely, traditional pay-TV subscription and on-demand revenue is anticipated to decline from $197.6 billion in 2022 to $177.5 billion in 2028.

To provide context within the broader media landscape, game revenue is projected to grow at a 2.9% CAGR over the forecast period, compared to 5.1% for the music sector and a robust 12.6% for cinema box office revenue.

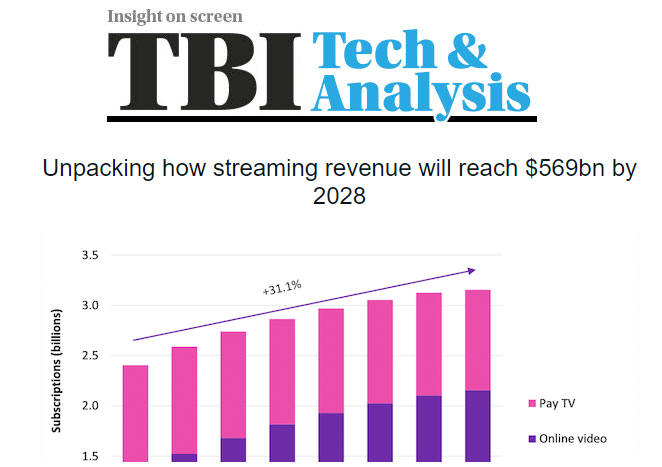

Online video subscriptions are on the rise. In 2021, there were 2.4 billion online video and pay-TV subscriptions worldwide, a number that climbed to nearly 2.6 billion in 2022. It is expected to surpass 2.7 billion by the end of 2023. Despite the industry’s focus on profitability, the appetite for TV and video consumption remains strong, and Omdia forecasts ongoing substantial growth, surpassing 3.1 billion subscriptions by the end of 2028.

Over the 2021–2028 period, TV/video combined subscription numbers will witness a growth of over 31%, with all the expansion driven by online video. Pay-TV subscriptions, on the other hand, are set to decrease by 7.4% during this period (from 1.079 billion to 999 million), while online video subscriptions will soar from 1.327 billion to 2.156 billion, marking a 62.5% increase.

While this continued growth in online video subscriptions paints a positive picture, it’s important to note that the increasing prevalence of lower Average Revenue Per User (ARPU) in online video subscriptions results in lower revenue growth compared to what would have been achieved with traditional pay-TV ARPU levels.

Pay-TV is experiencing a decline, with varying degrees of impact on different platforms. Cable-TV subscriptions are projected to decrease by 8.5% during 2021–2028, while satellite TV subscriptions are set to fall by 7.3%, and IPTV subscriptions are expected to rise by 10.6%.

These insights are excerpted from Omdia’s ‘Multisubscription TV & Video Forecast Report: 2015–28’, available for full access (subscription required). Adam Thomas, Senior Principal Analyst for TV & Online Video at Omdia, an Informa company, provides this valuable analysis.